Force Majeure Declared At Massive Grasberg Copper-Gold Mine Moves Copper Into Supply Deficit, Copper Soars 4%

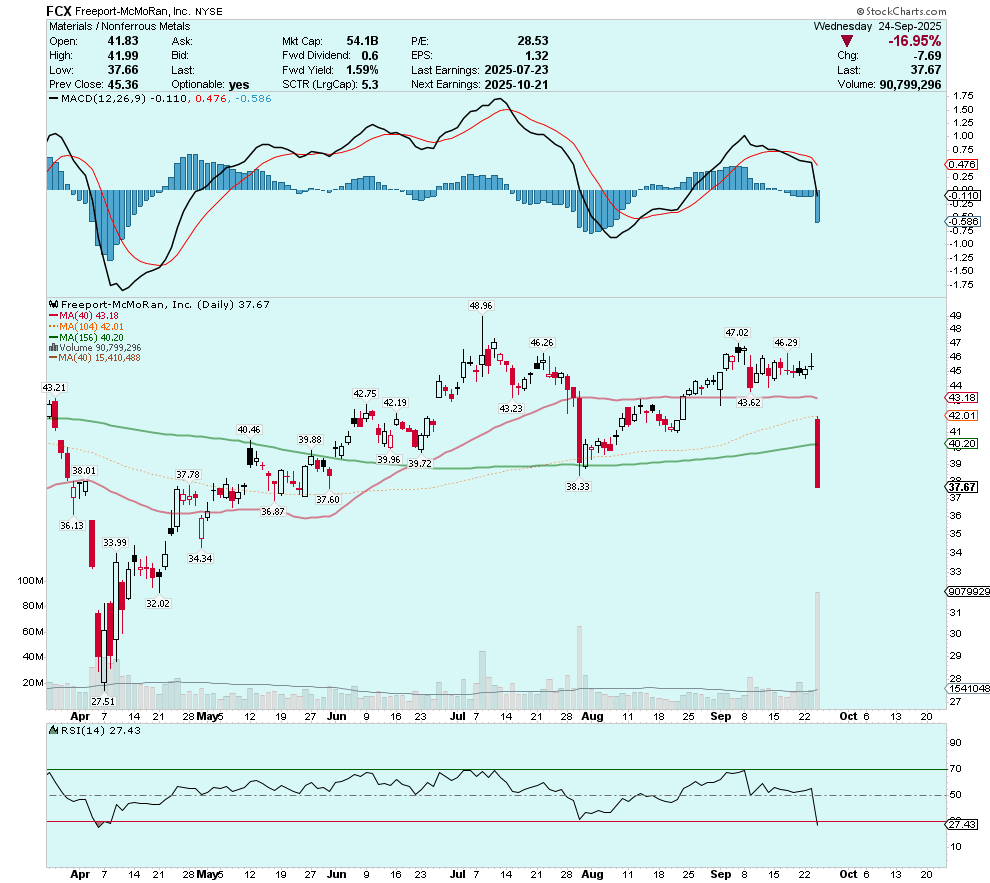

Shocking news from Indonesia sent Freeport-McMoRan shares tumbling 17%, chopping off US$11 billion from the mining giant's market cap.

Today’s news from Freeport-McMoRan (NYSE:FCX) sent FCX shares tumbling 17%, while copper futures rallied 4%.

FCX (Daily)

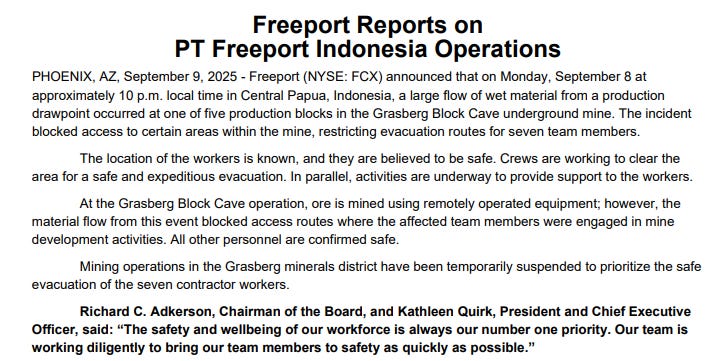

Before we delve into the longer term consequences of today’s force majeure news from Grasberg, I’d like to go back in time to September 9th when Freeport first reported “a large flow of wet material from a production drawpoint”.

It’s notable that the first communication regarding the mud flow at Grasberg Block Cave (GBC) focused on seven missing workers, who were “believed to be safe”. Mining operations were suspended to prioritize the safe evacuation of the workers, but there was no admission that there was damage to infrastructure and other production areas of the GBC. There was also no indication as to the tonnage of wet material.

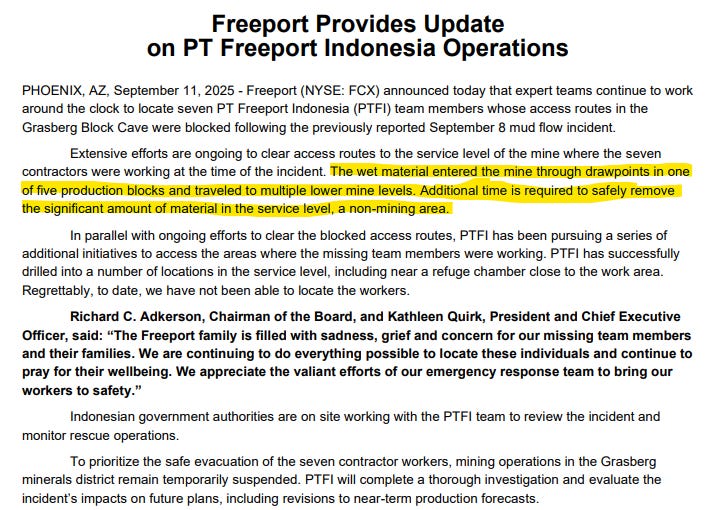

Two days later, FCX acknowledged that the wet material traveled to multiple lower mine levels but the focus was still on rescuing the trapped workers:

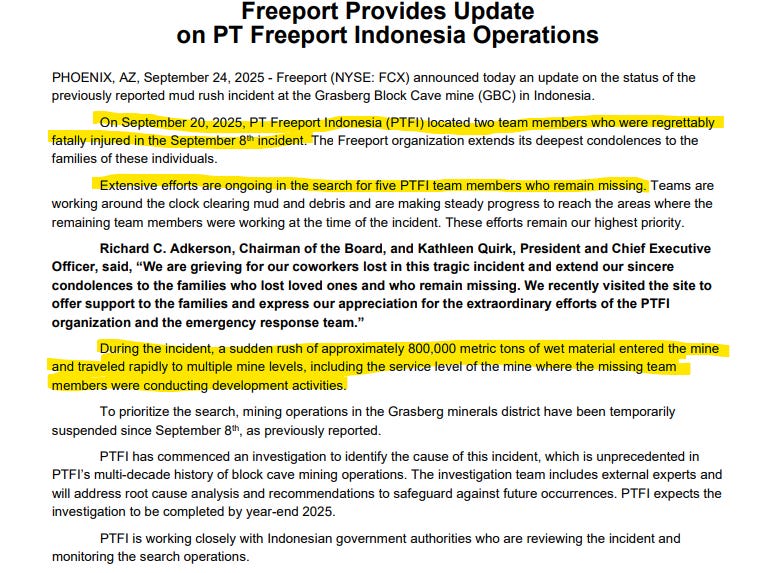

Today, FCX revealed that the bodies of two team members had been recovered and the rescue efforts are still ongoing to find the five missing workers.

At this point, sixteen days after the incident the outlook is dim for the missing five workers. Additionally, for the first time since the mud slide FCX decided that the disruption to mining operations is severe enough that it was forced to declare force majeure.

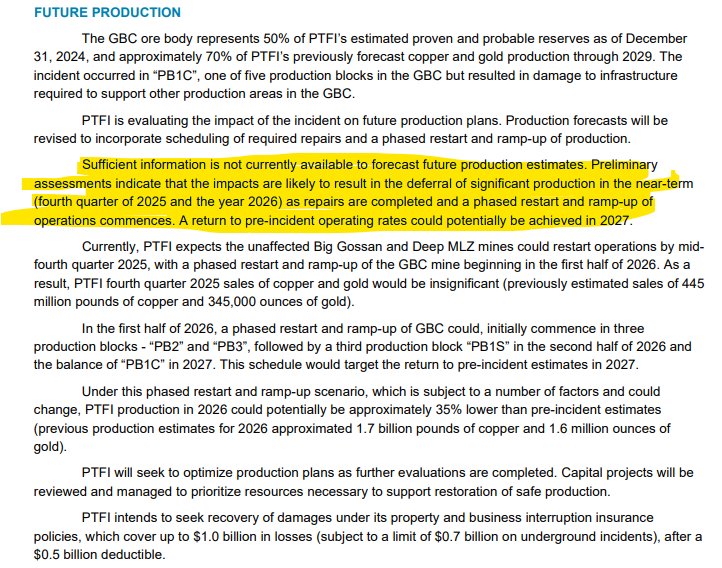

At this point, the damage to critical mine infrastructure at GBC is obviously substantial—the company plans to implement a thorough safety review, before eventually proceeding to a multi-phased resumption of operations beginning in 1H 2026.

The above highlighted paragraph was clearly a shock to the market; FCX is suddenly stating that the operation “could potentially” return to pre-incident operating rates in 2027. Moreover, 2026 production at PT Freeport Indonesia (full Grasberg mining complex including GBC) is forecast to be 600 million pounds of copper, and 560,000 ounces of gold less than the company’s previous guidance.

Additionally, FCX is basically resigning on Q4 2025 production stating that fourth quarter copper and gold sales will be “insignificant” (previously estimated sales of 445 million pounds of copper and 345,000 ounces of gold).

At this point, the incident at GBC is a very big deal. It has likely cost seven human lives, and sent one of the world’s largest copper and gold mines into a period of chaos. The closure of GBC for an extended period of time will have far reaching impacts on global copper supply & demand.

Morgan Stanley was quick to weigh in on the mounting global copper supply disruptions:

“Today’s Freeport news adds to ongoing supply disruptions, with WoodMac already calculating 3.7% or 900kt of disruptions as of August, suggesting room to overshoot the current allowance on a full year view. The new estimates imply a cut of 600 million pounds (270kt, or around 1.2% of mine supply) for 2026. This should tighten the deficit we already model for 2026 and brings upside risk to copper prices, with support from a weaker USD helping too.”

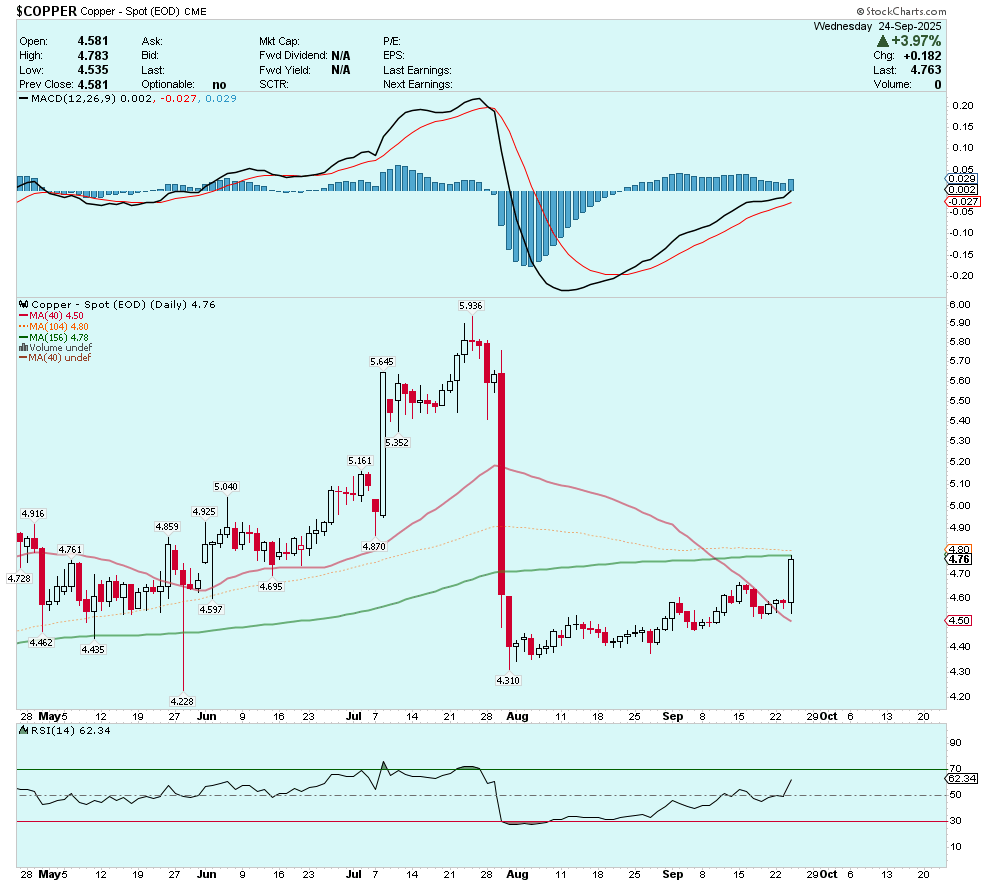

Copper (Daily)

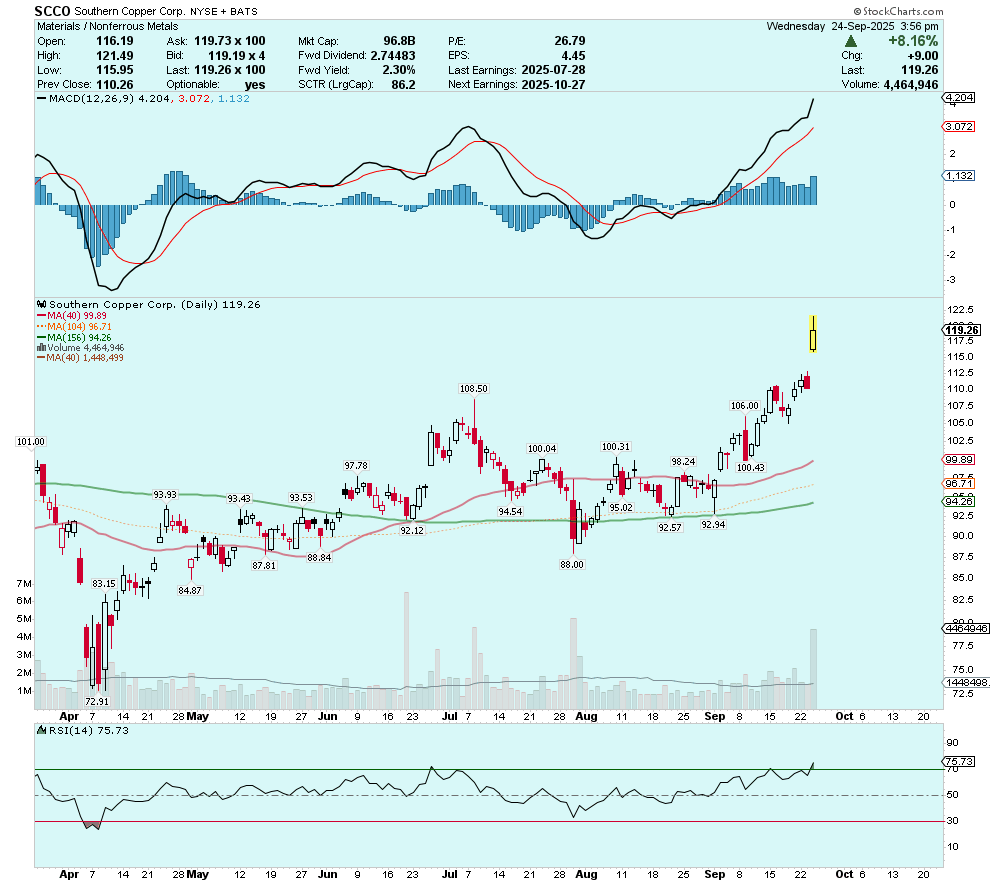

Let’s summarize what changed today and why other major copper producers saw their share prices react so favorably (SCCO +8.4%, HBM +5.8%, LUN +8.6%, Glencore +3% etc.):

Force majeure at Grasberg after a Sept 8 mud-rush (~800,000 tonnes of wet material), with mining in the district suspended to prioritize search and recovery. FCX cut Q3 sales guidance (-4% Cu; -6% Au) and said Q4 PTFI sales will be “insignificant.” Copper futures jumped ~4%.

Scale of the hit: The Grasberg district produced ~655 Mlb (297 kt) Cu in 1H25. FCX previously expected ~445 Mlb (~202 kt) Cu in Q4 from PTFI—now guided to near-zero; Q3 is trimmed by ~40 Mlb (~18 kt). That’s ~0.22 Mt less copper in 2025 vs July plans.

Impact on Global Copper Supply/Demand Balance

The ICSG had 2025 mine output growing to ~23.5 Mt (≈+2.3% y/y). Removing ~0.22 Mt from PTFI alone shaves ~1% of global mine supply this year—enough to deepen an existing deficit.

2026 is the bigger swing factor. Reporting today ranges from “no significant production throughout 2026; potentially back to pre-incident operating rate in 2027” to a phased GBC ramp starting 1H26 with Big Gossan/Deep MLZ restarting in Q4 2025. If GBC contributes little through 2026, the market could be short as much as 700,000 tonnes vs. previous expectations—~2–3% of world mine supply—a material, price-supportive shock.

Today’s shocking news from FCX strains an already tight global copper market. There is potential for the market to trade back up to the $5.00/lb level over the coming weeks, especially if supply issues persist (DRC floods, Chile incidents, Peru protests, etc.). We will also want to watch out for FCX’s detailed damage assessment & restart plan.

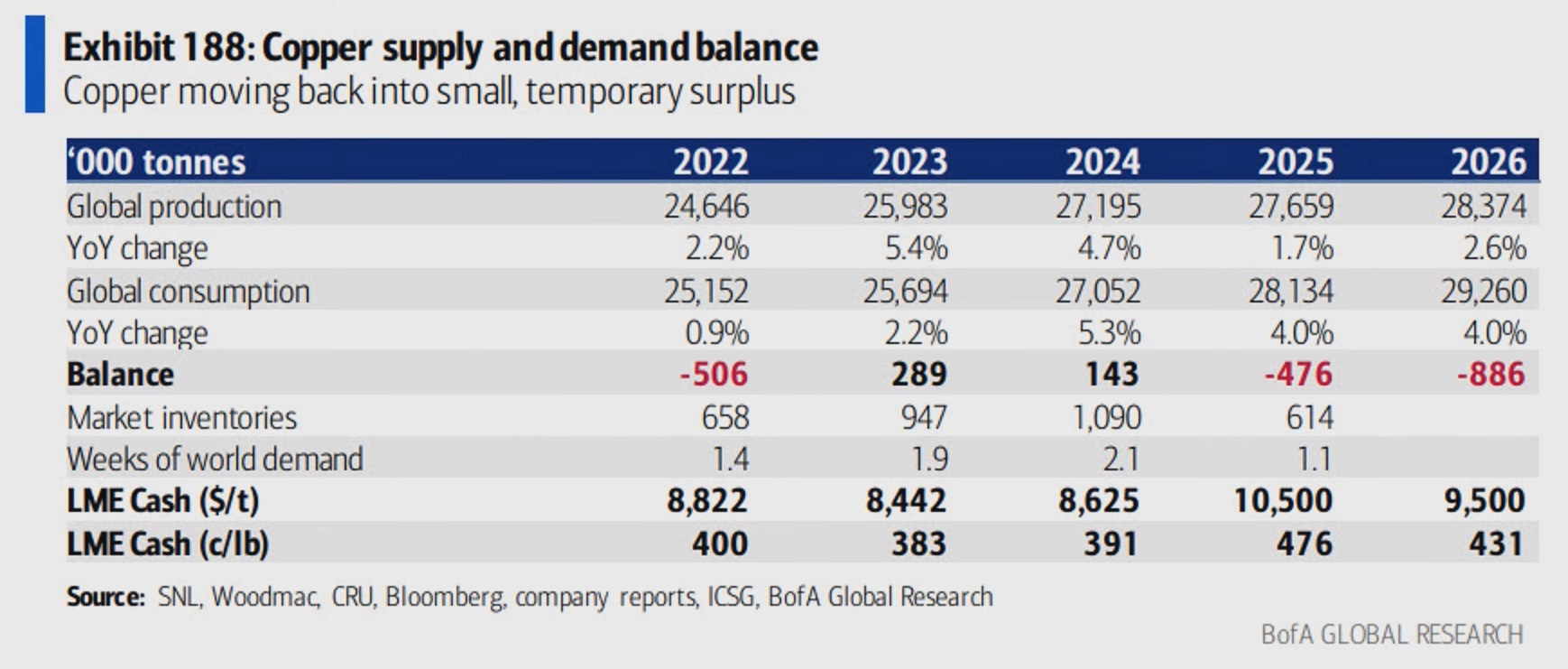

The global copper market was expected to be well-supplied in 2025, with most analysts forecasting a small surplus for the full year. However, where things get a lot more interesting is 2026 and beyond. Before today’s Grasberg force majeure there was a split among analysts as to whether the global copper market would be in a small surplus or deficit in 2026; JP Morgan forecast a deficit of 160,000 tonnes in 2026, whereas Macqarie saw a small surplus (less than 100,000 tonnes). However, after today’s news I expect to see a consensus form among analysts that copper will move to a significant deficit in 2026.

The above graphic is a year old, but it helps to illustrate the tight balance between global copper production and consumption.

The upside story for copper is structural, driven by sluggish mine supply struggling to keep pace with rising electrification and infrastructure demand. The supply deficit—expected to widen in 2026 and beyond—will only intensify the market’s growing appetite for copper.

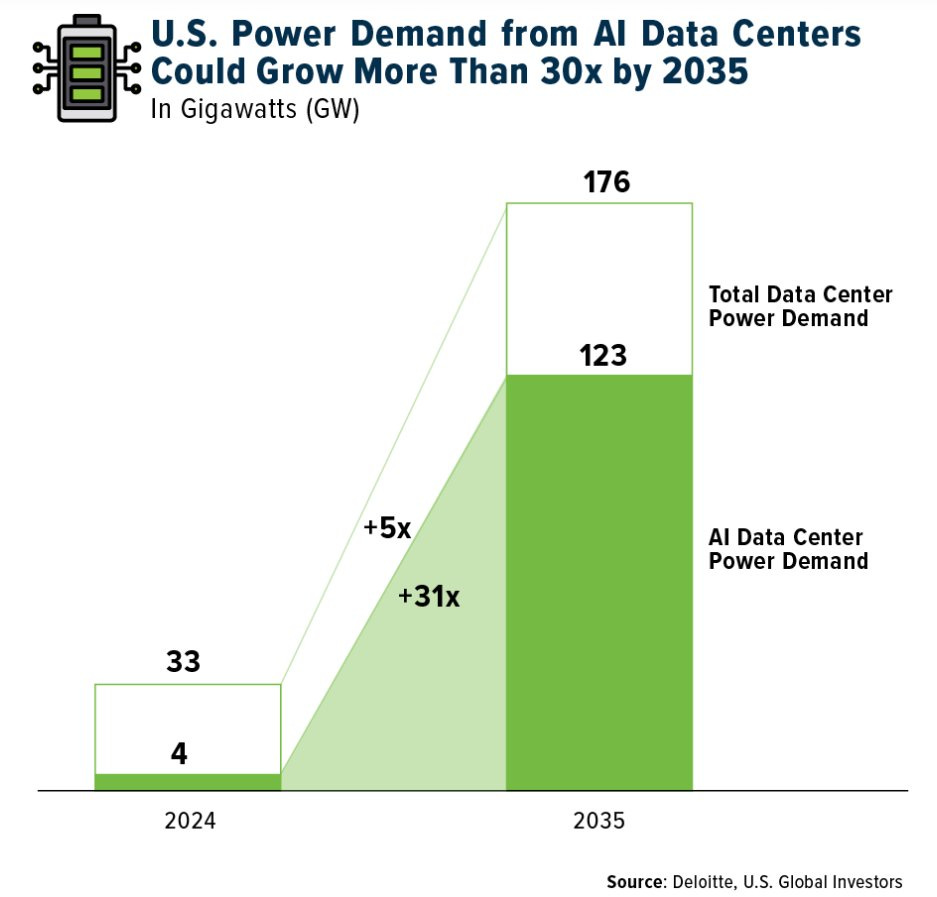

On average, a copper mine takes nearly 20 years to move from discovery to production. Meanwhile, AI-related demand for copper could reach 1 million tonnes (roughly 4% of global production) by 2030, as power consumption from data centers grows exponentially.

A global central bank easing cycle (underway) and a nascent China rebound (strengthened by continued fiscal stimulus and PBoC policy easing) could exacerbate the copper demand impulse, forcing prices to new highs. Earlier this year, we almost witnessed $6/lb, in 2026 we could see copper leap to $7/lb.

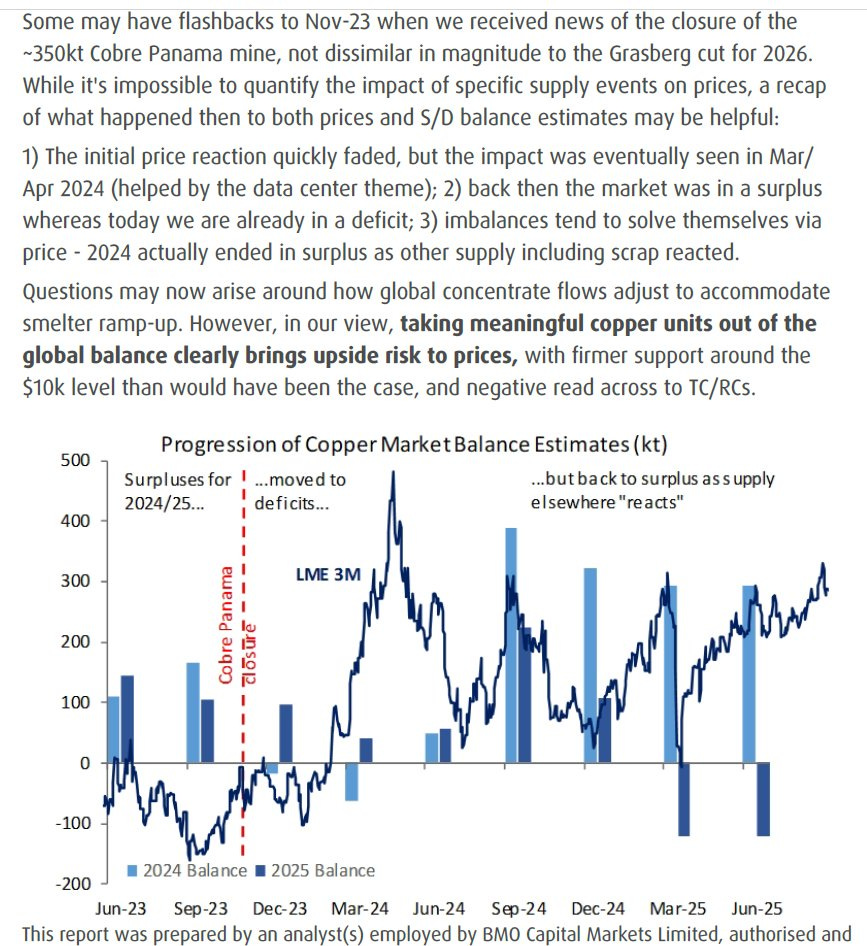

UPDATE: BMO compares the Grasberg force majeure news to the closure of Cobre Panama in November 2023

While today’s market moves in copper producers & developers was impressive, I could see more upside ahead in certain select names over the coming weeks.

Southern Copper (Daily)

Southern Copper (NYSE:SCCO) is a large copper producer (more than 2 billion pounds per year of copper production) that is on track to generate more than US$4 billion in free cash flow in 2025.

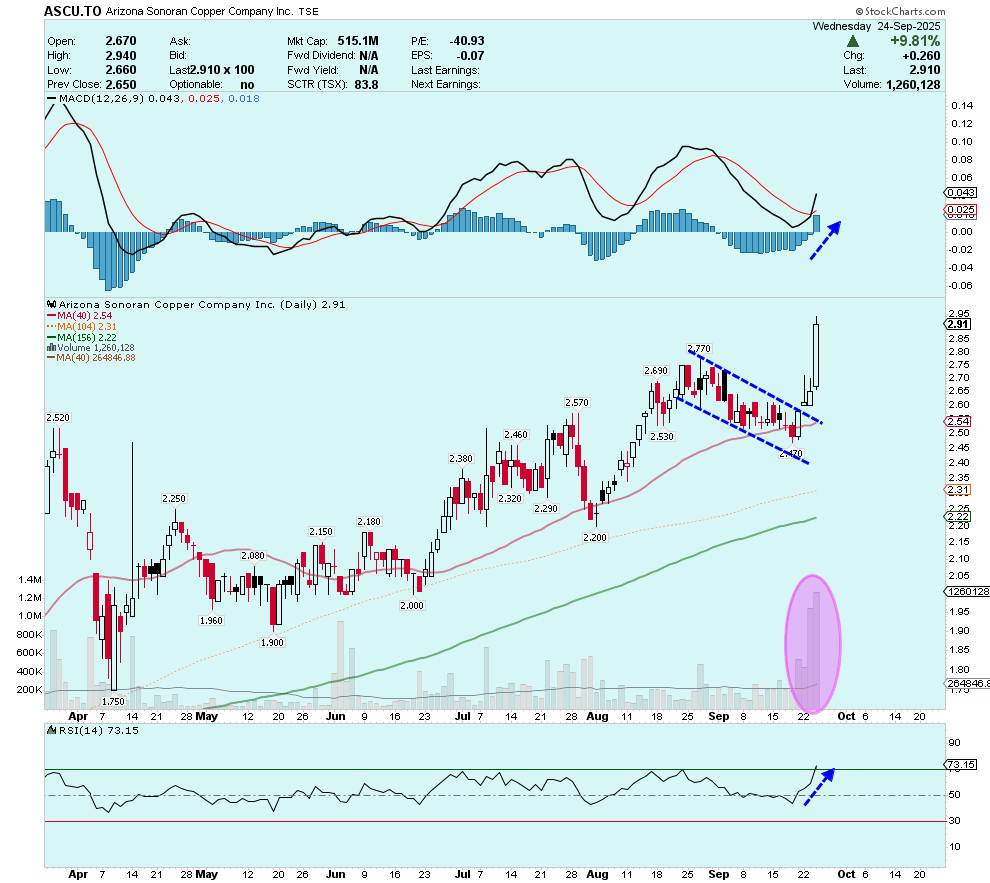

Arizona Sonoran Copper (Daily)

PFS imminent for Cactus following a strong updated Resource Estimate (11 billion pounds of contained copper, 75% of which is leachable).

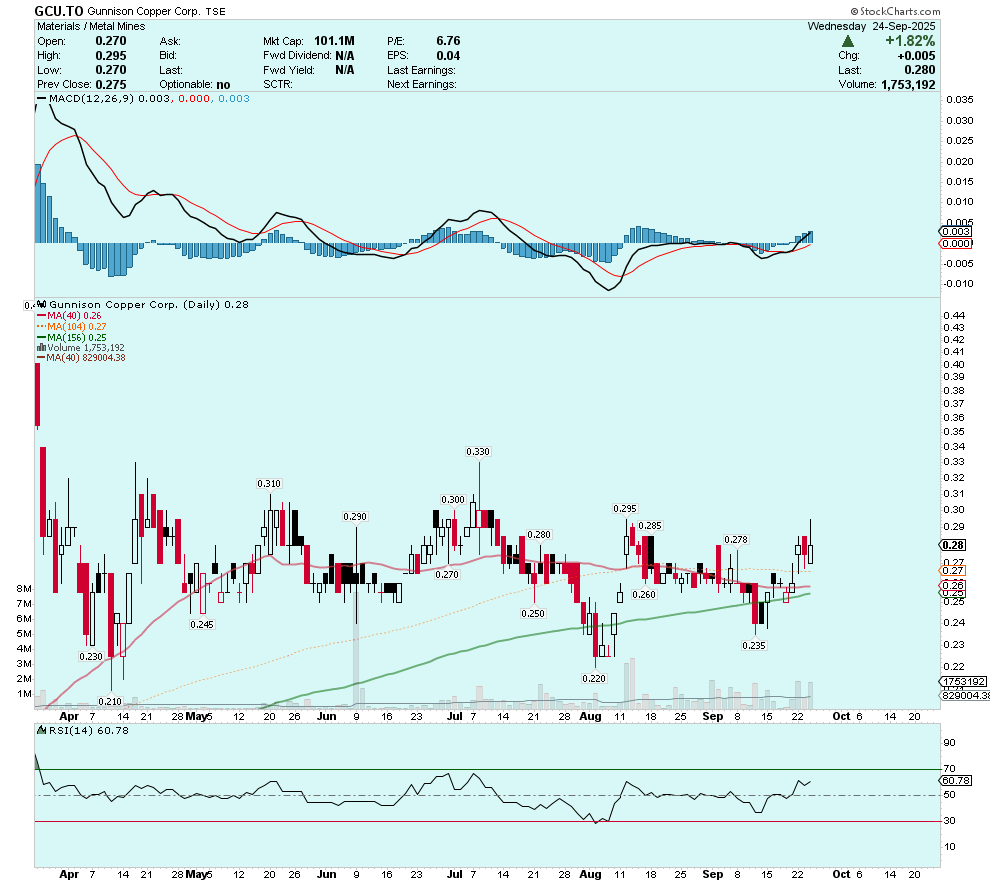

Gunnison Copper (Daily)

Continued production ramp-up at Johnson Camp along with high value-add programs in preparation for a prefeasibility study for the Gunnison Copper Project (open pit) in 2026.

Ivanhoe Electric (Daily)

Ivanhoe Electric (NYSE:IE) is targeting initial construction at Santa Cruz (NPV-8 = US$1.4 billion) in the first half of 2026, with first copper cathode production projected in 2028. The Santa Cruz Copper Project is poised to become one of the nation’s next major domestic producers of refined copper.

The premium on U.S. copper production is likely to persist, and potentially grow larger over time. Arizona Sonoran (Cactus), Ivanhoe Electric (Santa Cruz), and Gunnison Copper (Johnson Camp Mine and Gunnison Open Pit) are all uniquely positioned to deliver copper cathode production directly into the American domestic market via large-scale Arizona copper mining operations. Gunnison is already producing copper cathode at its Johnson Camp Mine (25 million lbs/annum nameplate capacity), while Ivanhoe Electric (first production in 2028) and Arizona Sonoran (first production in 2029) both have ambitious plans to be large-scale Arizona copper producers by 2030.

Disclosure: Author owns shares of ASCU.TO IE and GCU.TO at the time of publishing and may choose to buy or sell at any time without notice. Gunnison Copper has paid for the production and dissemination of corporate interviews.

DISCLAIMER: The work included in this article is based on current events, technical charts, company news releases, corporate presentations and the author’s opinions. It may contain errors, and you shouldn’t make any investment decision based solely on what you read here. This publication contains forward-looking statements, including but not limited to comments regarding predictions and projections. Forward-looking statements address future events and conditions and therefore involve inherent risks and uncertainties. Actual results may differ materially from those currently anticipated in such statements. This article is provided for informational and entertainment purposes only and is not a recommendation to buy or sell any security. Always thoroughly do your own due diligence and talk to a licensed investment adviser prior to making any investment decisions. Junior resource companies can easily lose 100% of their value so read company profiles on www.SEDAR.com for important risk disclosures. It’s your money and your responsibility.