Gold Sees Largest Weekly Outflow After Barron's "Gold Rush" Cover: How To Keep Your Eye On The Ball

Barron's can oftentimes have uncanny timing with its magazine covers, last week was no exception.

Barron’s can have remarkable timing with some of its covers, last weekend’s gold cover was no exception:

The week before last week’s Barron’s cover, gold reached $3,509/oz and proceeded to print a ‘shooting star’ candlestick on the weekly chart:

Gold (Weekly)

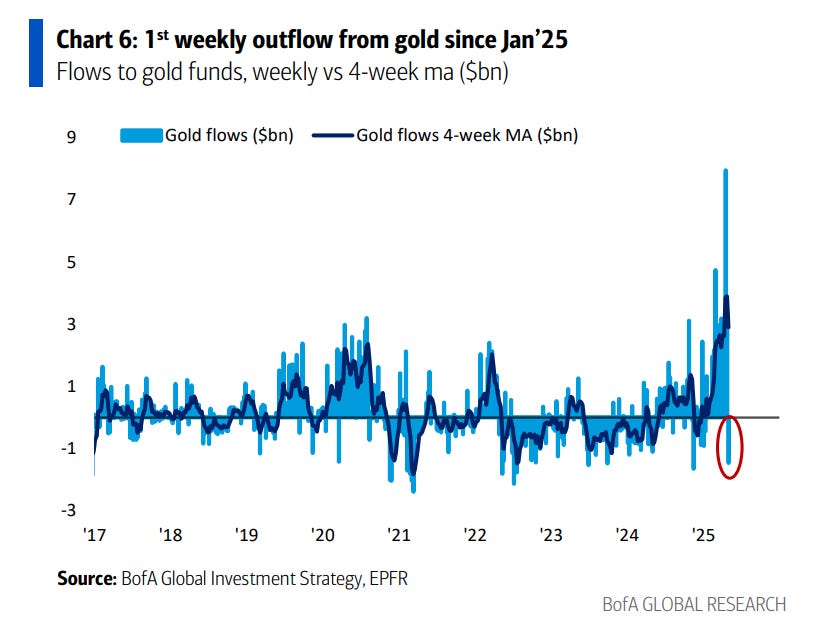

Last week, gold fell ~2.5% and gold ETFs saw their first weekly outflow since January:

After feverish inflows into gold funds in early April, it wasn’t terribly unexpected to see some profit taking kick in. Despite the fact that the Barron’s article wasn’t overwhelmingly bullish (and actually emphasized that gold should not be expected to outperform stocks), some investors may have hit the sell button assuming that a Barron’s cover coming on the back of a 30% YTD gain couldn’t be a better sign to take profits.

Additionally, we’ve seen the US dollar firm a bit and Treasury yields begin to rise. Traditionally, we would expect gold to correct against a backdrop of a firmer dollar and rising yields. And so it has.

During a seasonally weak time of year for gold (May/June) there is certainly potential for a deeper correction to materialize. However, we shouldn’t lose sight of the bigger picture and the seismic shifts that are underway across the global financial & trading systems.

This weekend in Omaha, Warren Buffett dropped a soundbite that caught some attention:

BUFFETT SAYS THERE COULD BE THINGS THAT WOULD HAPPEN IN US THAT WOULD "MAKE US WANT TO OWN A LOT OF OTHER CURRENCIES"

What are those things Warren? Perhaps messing with Federal Reserve independence? Or perhaps using taxpayer money to create a cryptocurrency reserve fund? Or maybe using tariffs as a weapon to threaten other countries including some of the USA’s closest allies?

It is out of the ordinary for Mr. Buffett to offer much commentary on currencies. Historically, he has rarely gone too far astray from holding US dollars.

Berkshire Hathaway holds more than $300 billion in US T-Bills, so Buffett’s words regarding diversifying into other currencies should not be taken lightly.

Trump says he knows more about interest rates than Fed Chairman Jerome Powell. That assertion is highly debatable. However, it’s not debatable that the most successful investor in history knows a helluva lot more than Trump about just about everything, especially interest rates and currencies.

After embarking on a pretty fierce assault on Powell a couple weeks ago, Trump has calmed his tone recently. However, one has to wonder how long this relative calm will last.

What happens if the labor market continues to soften and market turmoil resumes this summer?

It is not a secret that Trump wants interest rates lower, he would also prefer to see a weaker dollar in order to help strengthen the US export sector and rebalance the current large trade imbalances.

It remains to be seen whether Trump 2.0 will stay committed to its aggressive tariff policy on China. As it stands now the stock market has started calling Trump’s bluff and begun pricing in some sort of pause or ratcheting lower of the tariffs on China.

While China is the elephant in the room, it is unclear whether the US will be able to make substantive progress in trade deals with ‘allies’ like the EU or Japan; Japan is pushing back hard on autos and steel tariffs, meanwhile the list of trade disagreements between the US and EU is longer than the Bible.

I can’t handicap how the Trump 2.0 tariffs will play out. Frankly, I don’t think anyone can, not even Trump himself. However, I can confidently state that in the last few months the US has lost some of its prestige in the eyes of much of the world. Trust has been damaged and de-dollarization is back at the forefront of the conversation for many investors globally.

During more chaotic macro-market episodes, I find it especially valuable to refocus on longer term trends and investment themes. I believe that one of the most important themes of this final chapter of the Fourth Turning (2025-2030?) will be the decline of the US dollar as the global reserve currency.

A 40-year monthly chart of the US Dollar Index helps to put things into perspective:

US Dollar Index (Monthly)

In the above chart, please note the strong negative correlations between the USD and gold during the late 1980s and early 2000s US dollar bear markets.

Since 1985, the US dollar has been gradually moving lower - this downtrend includes a major low in 1992 (following a recession), a major peak in Q1 2002, and a major low in 2008 (as the GFC erupted).

Over the last few years, the US Dollar Index may have hammered out a critical multi-year topping process. Within the context of the 40-year chart, this multi-year topping process is simply another lower high.

The dollar strength of the last few years was bolstered by tightening Federal Reserve monetary policy and a period of so called “US Exceptionalism”. As the Fed gradually transitions from a restrictive posture to a more accommodative posture (beginning last year), and the illusion of US exceptionalism begins to wash away, it makes sense that the US dollar would resume its longer term downtrend.

The next leg of the US dollar bear market could see the US Dollar Index decline below its 2008 low (71.80).

The Trump 2.0 term lasts until January 2029. Considering some of Trump 2.0’s policy objectives and strong desire for a more ‘accommodative’ Federal Reserve Chair, it is within the realm of possibility that the US dollar could reach fresh all-time lows during the next four years.

A US economic recession could prove to be very negative for the US dollar. After all, if US real rates move back into negative territory while real GDP growth is negative, and fiscal deficits remain at > 5% of GDP levels, the dollar will no longer look like the “cleanest dirty shirt in the laundry”.

Even in a scenario in which the US economy avoids recession, the desire of the Executive Branch to reduce interest rates and weaken the dollar is likely to assert itself - even if this desire has to remain patient until the summer of 2026 (when Trump can appoint a new Fed Chair).

Gold stands to play an increasingly prominent role as a monetary metal, and an alternative currency on the global stage.

If we do experience a deeper correction in gold over the coming weeks, I implore readers to view it for what it is: A healthy reset, and a buying opportunity within the context of a long term secular bull market.

The chart of total shares outstanding in the GLD exchange-traded fund is another picture that helps to put things into perspective, and keep our eye on the ball:

Unlike the 2004-2011 and 2018-2020 gold bull cycles, the first stage of gold’s latest bull market move (since October 2022) saw GLD’s outstanding shares shrink. This is strong evidence that North American investors did not participate in gold’s rise from Q4 2022 through Q2 2024. It has really only been since the beginning of this year that we have seen strong evidence of participation from North American and European investors. The above chart is not indicative of a top. If anything, it tells me that this gold bull market cycle has at least another year left.

The Barron’s cover may have helped to signal a short term emotional extreme in the gold market. But make no mistake, the gold bull has never been stronger. The April gold rally was so powerful that it became too much a good thing. I view a correction as a welcome, and healthy gift.

DISCLAIMER: The work included in this article is based on current events, technical charts, company news releases, corporate presentations and the author’s opinions. It may contain errors, and you shouldn’t make any investment decision based solely on what you read here. This publication contains forward-looking statements, including but not limited to comments regarding predictions and projections. Forward-looking statements address future events and conditions and therefore involve inherent risks and uncertainties. Actual results may differ materially from those currently anticipated in such statements. This article is provided for informational and entertainment purposes only and is not a recommendation to buy or sell any security. Always thoroughly do your own due diligence and talk to a licensed investment adviser prior to making any investment decisions. Junior resource companies can easily lose 100% of their value so read company profiles on www.SedarPlus.ca for important risk disclosures. It’s your money and your responsibility.