While Gold Closes In On $3,000/oz A Very Weird Gold Market Sees Outflows From GDX

Yesterday, at the BMO Metals & Mining Conference Ross Beaty called the current market environment "a very weird gold market"

Yesterday, billionaire mining entrepreneur did an interview at the BMO Metals & Mining Conference in which he said the following:

“You know it's a very weird gold market right now, Paul, as we talked about last time we were together, you have this absolutely bizarre disconnect between the gold price which is at a record high $2900 an ounce, and has just been on wheels for the last year, and the gold equities which are still trading as if gold was $1,800 an ounce. There just has not been money pouring into that equity space because the buyers of gold are a different group of entities than buyers of equities.”

The primary buyers of gold globally continue to be central banks. Central banks do not buy mining stocks. Therein lies the simplest explanation for why the gold mining sector has delivered an underwhelming performance despite gold’s ascent from ~$2,000/oz in January 2024 to nearly $3,000/oz today.

However, the fact remains that the value of the product the gold mining industry produces has appreciated substantially in the last year. Yet, the price of many large gold producer shares (looking at you Barrick and Newmont) has not reciprocated gold’s performance.

Why is this?

I cannot count the number of times I have been asked a similar question in recent months. In fact, just last night I was asked this question again in a response to an X tweet on Ross Beaty’s interview quote:

Companies as big as Barrick and Newmont are dealing with enormous amounts of operational complexity. They have operations stretching across continents, and each mine has an enormous amount of multi-layered complexity in itself. The supply chain disruptions and inflation surge of 2021-2023 thoroughly tested the large producers, creating some disappointing financial performance in the process. It was during this period that many investors experienced their final disillusionment with the mining sector.

So far, the gold price performance hasn’t been enough to motivate these investors to return:

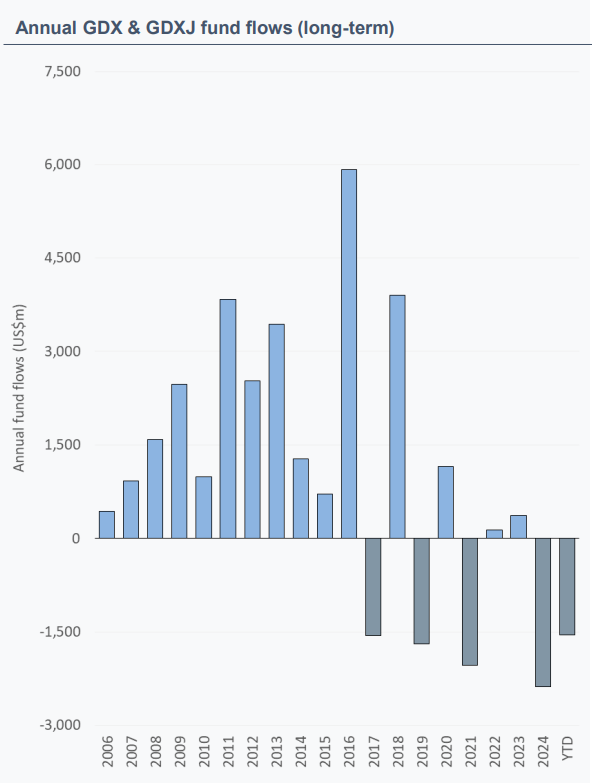

The large and highly liquid GDX and GDXJ exchange-traded funds have experienced outflows to the tune of a few billion dollars during a period of market history in which gold has repeatedly made new all-time highs, rising to levels some didn’t think possible.

Again, we have to remind ourselves that most of the buyers of 400-ounce gold bars are not part of the potential investor pool for gold mining stocks. In addition, gold mining is a tough business. Despite generating record levels of free cash flow in Q4 2024, the latest set of quarterly earnings reports from the major producers included 2025 guidance that pointed to lower production, higher costs, and higher capex vs. consensus expectations and their respective 2024 results.

This is a problem.

The gold price rally is fantastic, and it is fuel for much stronger financial performance from the sector. However, the reality is that higher costs and lower production are not going to cause Wall Street hedge fund managers to trip over one another to buy the GDX.

The gold mining sector needs more consolidation and more world class discoveries. The latter is very hard to achieve, the former is possible and exceedingly likely to play out over the next year.

There is no reason we can’t have a $100 billion market cap gold producer. There is also no reason to have a bunch of single asset producers out there. The cost of capital is too high for these small producers, and the risk is enormous.

The good news is that the balance sheets of the large producers have never been better and profitability of the sector has also never been better. In spite of investor sentiment, the gold mining sector has rarely been in the position of strength it finds itself in today.

DISCLAIMER: The work included in this article is based on current events, technical charts, company news releases, corporate presentations and the author’s opinions. It may contain errors, and you shouldn’t make any investment decision based solely on what you read here. This publication contains forward-looking statements, including but not limited to comments regarding predictions and projections. Forward-looking statements address future events and conditions and therefore involve inherent risks and uncertainties. Actual results may differ materially from those currently anticipated in such statements. This article is provided for informational and entertainment purposes only and is not a recommendation to buy or sell any security. Always thoroughly do your own due diligence and talk to a licensed investment adviser prior to making any investment decisions. Junior resource companies can easily lose 100% of their value so read company profiles on www.SEDARplus.ca for important risk disclosures. It’s your money and your responsibility.